On October 26th, I made what was to be a highly contentious bearish call on the SPDR Gold Trust ETF (GLD) in my article GLD: Sell While You Still Have A Chance. As is often the case with negative outlooks for precious metals, the article was met with nearly unanimous opposition. Most of this uni-directional response came from readers with stated long positions in gold and its correlated assets, so I suppose it could be said that I should not have expected anything different. In an effort to be as specific as possible (something I feel is missing in most publications) I went on to offer exact price targets to the downside, as explained in my follow-up GLD: Bears Set Sights On 115. After nailing the cyclical top on October 26th (to the day),valuations in GLD dropped 12% in less than two months en route to this target, with very little to be seen in terms of upside correction. Clearly-Defined Bearish EnvironmentFrom a fundamental perspective, all of my scenarios played out exactly as expected. Demand in emerging markets has not been enough to counteract the oppositional effects of a strengthening U.S. Dollar, and GDP results have consistently surpassed consensus estimates. We have seen several examples of some of the market's biggest gold bugs (John Paulson (Trades, Portfolio), along with others) bailing out on their previously established outlooks, cutting their losses and reversing positions. The unfortunate reality for many investors with long positions in precious metals, however, has been much more difficult to accept. Costly (and completely avoidable) losses have come as a result, and the psychological forces that seem to govern the gold markets can only be described in one way: When you're right, you're still wrong if you are negative on precious metals. B! ut now we are seeing that this isn't the case.Fed Tapering Confirmed by Employment, GDP PerformancesOf course, markets never reward investments that are governed by emotion and psychological responses. In gold, investors will need to start accepting the fact that gold no longer holds the safe-haven, alternative store of value position it once had. The macroeconomic environment simply does not support the argument for sustainable gold prices at current levels. Those that have suggested the Fed will never be able to start tapering have already been proven wrong, and the bullish outlook for the broader economy is now being confirmed by the latest performances in U.S. GDP:

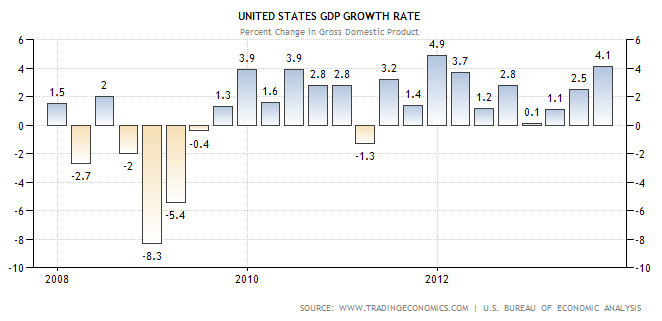

Clearly-Defined Bearish EnvironmentFrom a fundamental perspective, all of my scenarios played out exactly as expected. Demand in emerging markets has not been enough to counteract the oppositional effects of a strengthening U.S. Dollar, and GDP results have consistently surpassed consensus estimates. We have seen several examples of some of the market's biggest gold bugs (John Paulson (Trades, Portfolio), along with others) bailing out on their previously established outlooks, cutting their losses and reversing positions. The unfortunate reality for many investors with long positions in precious metals, however, has been much more difficult to accept. Costly (and completely avoidable) losses have come as a result, and the psychological forces that seem to govern the gold markets can only be described in one way: When you're right, you're still wrong if you are negative on precious metals. B! ut now we are seeing that this isn't the case.Fed Tapering Confirmed by Employment, GDP PerformancesOf course, markets never reward investments that are governed by emotion and psychological responses. In gold, investors will need to start accepting the fact that gold no longer holds the safe-haven, alternative store of value position it once had. The macroeconomic environment simply does not support the argument for sustainable gold prices at current levels. Those that have suggested the Fed will never be able to start tapering have already been proven wrong, and the bullish outlook for the broader economy is now being confirmed by the latest performances in U.S. GDP: Driven largely by surges in consumer spending, GDP growth for the third quarter is now seen expanding at a rate of 4.1%, which is its fastest rate in two years and well above the market's initial estimates. These improvements match the trajectory that is seen in labor markets as well (with the unemployment rate now on track to fall below 7%). Second quarter GDP came in at 2.5%, so the progress here is clear, as are the market's erroneous estimates discounting the true strength that is building in theU.S. economy. These figures help support the Fed's decision last week to begin tapering its quantitative easing stimulus programs -- in a move that was long overdue.Correlated Assets: Don't Forget the Dollar

Driven largely by surges in consumer spending, GDP growth for the third quarter is now seen expanding at a rate of 4.1%, which is its fastest rate in two years and well above the market's initial estimates. These improvements match the trajectory that is seen in labor markets as well (with the unemployment rate now on track to fall below 7%). Second quarter GDP came in at 2.5%, so the progress here is clear, as are the market's erroneous estimates discounting the true strength that is building in theU.S. economy. These figures help support the Fed's decision last week to begin tapering its quantitative easing stimulus programs -- in a move that was long overdue.Correlated Assets: Don't Forget the Dollar These developments bode well for expected performances in the U.S. Dollar, and in assets like the PowerShares DB U.S. Dollar Index Bullish ETF (UUP). Of c! ourse, th! e opposite is then true for inversely-correlated assets like GLD. When we compare the relative GDP performance in the U.S. to what is seen elsewhere (for example, in Japan, the U.K., and in the eurozone), a clearly bullish scenario starts to emerge and support the argument for continued strength in the U.S. dollar.GLD: Chart Perspective

These developments bode well for expected performances in the U.S. Dollar, and in assets like the PowerShares DB U.S. Dollar Index Bullish ETF (UUP). Of c! ourse, th! e opposite is then true for inversely-correlated assets like GLD. When we compare the relative GDP performance in the U.S. to what is seen elsewhere (for example, in Japan, the U.K., and in the eurozone), a clearly bullish scenario starts to emerge and support the argument for continued strength in the U.S. dollar.GLD: Chart Perspective All of these factors will continue to weigh on gold into next year. I should say that I believe it is time to take profits on short positions in GLD, however, as the recent moves (since my bearish call on October 26th) have been forceful and we are in need of some short-term corrective retracement. Upside will remain limited, though, and a monthly close below 115 would signal a sea change in the precious metals markets. Long-term bulls should proceed with caution.About the author:RichardCoxRichard Cox is a university teacher in international trade and finance. Lecture halls of 80 to 120 students. Lessons in macroeconomics and price behavior in equity markets. Investing strategies in these articles are based on technical and fundamental analysis of all the major asset classes (stocks, commodities, currencies). Trade ideas are generally based on time horizons of one to six months. Follow me on Twitter: @Richard_A_Cox

All of these factors will continue to weigh on gold into next year. I should say that I believe it is time to take profits on short positions in GLD, however, as the recent moves (since my bearish call on October 26th) have been forceful and we are in need of some short-term corrective retracement. Upside will remain limited, though, and a monthly close below 115 would signal a sea change in the precious metals markets. Long-term bulls should proceed with caution.About the author:RichardCoxRichard Cox is a university teacher in international trade and finance. Lecture halls of 80 to 120 students. Lessons in macroeconomics and price behavior in equity markets. Investing strategies in these articles are based on technical and fundamental analysis of all the major asset classes (stocks, commodities, currencies). Trade ideas are generally based on time horizons of one to six months. Follow me on Twitter: @Richard_A_Cox

Visit RichardCox's Website

| Currently 0.00/512345 Rating: 0.0/5 (0 votes) | |

No comments:

Post a Comment