Alamy Tax season is a time of stress for many, but it can be a joyful time for the roughly 75 percent of Americans who receive income tax refunds. While the refund really means you're getting back money you loaned to the government at no interest, in practical terms it often means an unexpected infusion of cash into your wallet or bank account. Last year's average income tax refund was $2,755, according to the Internal Revenue Service. That's a nice chunk of change. It's a great problem to have: What do you do with your windfall? The best choice for one person may not be the best choice for another. But experts agree on one thing: If you have debt, apply your refund to paying it off, whether it's credit card debt, student loan debt or other consumer debt. "People should still be focusing first on paying down debt," says Meisa Bonelli, a Wall Street finance and tax professional whose Millennial Tax company advises entrepreneurs on business and tax strategy. Debt, particularly student loan debt, should be a primary target because it limits financial options, preventing people from doing what they want with their money, whether it's buying a house, buying a car or taking a vacation. "Get that debt gone," she says. "It holds you back from everything else you want to do in life." Eric Rosenberg, a financial analyst who writes the blog Narrow Bridge Finance, agrees. "The No. 1 thing anyone should do with a tax refund is pay down debt," he says. After he left graduate school with $40,000 in student loan debt, he focused on aggressively paying it off. Using all his tax refunds and bonuses, he made the final payment just two years and six days after his graduation. With his student loan debt cleared away, he began saving his tax refunds, with the goal of buying a home. He didn't apply any of his refund money to splurges -- instead, he saved for fun and vacation with his regular income. The refunds were earmarked for bigger things. "I treated it like it was extra money that I didn't need to live on," Rosenberg says. "I always encourage people to think long term, not short term." Others believe that giving yourself license to splurge with part of your refund helps you save the rest. Stephanie Halligan, a financial consultant and blogger, signs a contract with herself before she does her taxes, allocating 50 percent of her refund to student loans and 25 percent to long-term savings. She can spend the remaining 25 percent on whatever she wants. "It's easy to react on impulse and emotion when your refund hits, so prepare now for what you'll do with that moolah later," she advises on her personal finance website, The Empowered Dollar. If you're getting a big refund -- a check in the ballpark of $1,000 or more for taxpayers who don't have a side business -- consider adjusting your withholding so that you'll have that money available to you during the year. But those who don't have substantial savings want to avoid a scenario in which they owe four figures to the IRS at tax time. "I think people should withhold the maximum they can withhold," Bonelli says. Rosenberg concurs. As his businesses, running Narrow Bridge Finance and building websites, have grown, his refunds have shrunk. Last year he had to pay the IRS. Here are the seven smartest things you can do with your refund: Pay down debt. If you have any consumer debt -- student loans, credit card balances or installment loans -- pay those off before using your refund for any other purpose. Car payments and home mortgages aren't in this category, but you can consider paying extra principal. Add to your savings. "You can never save enough," Bonelli says. You can use the money to build up your emergency fund, your kids' college funds or put it toward a specific goal, such as buying a house or a car or financing a big vacation. Add to your retirement accounts. If you put $2,500 from this year's tax refund into an IRA, it would grow to $8,500 in 25 years, even at a modest 5 percent rate of return, TurboTax calculates. If you saved $2,500 every year for 25 years, you'd end up with more than $130,000 at that same 5 percent rate of return. Invest in yourself. This could mean taking a class in investing, studying something that interests you or even taking a big trip. "Do something that enriches yourself or adds value to your life," Bonelli says. She is planning to take a class in art therapy this year using money from her refund. Improve your home. Consider putting your refund to good use by adding insulation, replacing old windows and doors or other improvements that would save energy, and therefore money. Or perhaps it's time to remodel your bathroom or kitchen. You're adding value to your home at the same time you're improving your living experience. Apply your refund toward next year's taxes. This is common among self-employed taxpayers, who are required to pay quarterly taxes since they don't have taxes withheld. By applying any overpayment toward upcoming tax payments, you can free up other cash.

Alamy Tax season is a time of stress for many, but it can be a joyful time for the roughly 75 percent of Americans who receive income tax refunds. While the refund really means you're getting back money you loaned to the government at no interest, in practical terms it often means an unexpected infusion of cash into your wallet or bank account. Last year's average income tax refund was $2,755, according to the Internal Revenue Service. That's a nice chunk of change. It's a great problem to have: What do you do with your windfall? The best choice for one person may not be the best choice for another. But experts agree on one thing: If you have debt, apply your refund to paying it off, whether it's credit card debt, student loan debt or other consumer debt. "People should still be focusing first on paying down debt," says Meisa Bonelli, a Wall Street finance and tax professional whose Millennial Tax company advises entrepreneurs on business and tax strategy. Debt, particularly student loan debt, should be a primary target because it limits financial options, preventing people from doing what they want with their money, whether it's buying a house, buying a car or taking a vacation. "Get that debt gone," she says. "It holds you back from everything else you want to do in life." Eric Rosenberg, a financial analyst who writes the blog Narrow Bridge Finance, agrees. "The No. 1 thing anyone should do with a tax refund is pay down debt," he says. After he left graduate school with $40,000 in student loan debt, he focused on aggressively paying it off. Using all his tax refunds and bonuses, he made the final payment just two years and six days after his graduation. With his student loan debt cleared away, he began saving his tax refunds, with the goal of buying a home. He didn't apply any of his refund money to splurges -- instead, he saved for fun and vacation with his regular income. The refunds were earmarked for bigger things. "I treated it like it was extra money that I didn't need to live on," Rosenberg says. "I always encourage people to think long term, not short term." Others believe that giving yourself license to splurge with part of your refund helps you save the rest. Stephanie Halligan, a financial consultant and blogger, signs a contract with herself before she does her taxes, allocating 50 percent of her refund to student loans and 25 percent to long-term savings. She can spend the remaining 25 percent on whatever she wants. "It's easy to react on impulse and emotion when your refund hits, so prepare now for what you'll do with that moolah later," she advises on her personal finance website, The Empowered Dollar. If you're getting a big refund -- a check in the ballpark of $1,000 or more for taxpayers who don't have a side business -- consider adjusting your withholding so that you'll have that money available to you during the year. But those who don't have substantial savings want to avoid a scenario in which they owe four figures to the IRS at tax time. "I think people should withhold the maximum they can withhold," Bonelli says. Rosenberg concurs. As his businesses, running Narrow Bridge Finance and building websites, have grown, his refunds have shrunk. Last year he had to pay the IRS. Here are the seven smartest things you can do with your refund: Pay down debt. If you have any consumer debt -- student loans, credit card balances or installment loans -- pay those off before using your refund for any other purpose. Car payments and home mortgages aren't in this category, but you can consider paying extra principal. Add to your savings. "You can never save enough," Bonelli says. You can use the money to build up your emergency fund, your kids' college funds or put it toward a specific goal, such as buying a house or a car or financing a big vacation. Add to your retirement accounts. If you put $2,500 from this year's tax refund into an IRA, it would grow to $8,500 in 25 years, even at a modest 5 percent rate of return, TurboTax calculates. If you saved $2,500 every year for 25 years, you'd end up with more than $130,000 at that same 5 percent rate of return. Invest in yourself. This could mean taking a class in investing, studying something that interests you or even taking a big trip. "Do something that enriches yourself or adds value to your life," Bonelli says. She is planning to take a class in art therapy this year using money from her refund. Improve your home. Consider putting your refund to good use by adding insulation, replacing old windows and doors or other improvements that would save energy, and therefore money. Or perhaps it's time to remodel your bathroom or kitchen. You're adding value to your home at the same time you're improving your living experience. Apply your refund toward next year's taxes. This is common among self-employed taxpayers, who are required to pay quarterly taxes since they don't have taxes withheld. By applying any overpayment toward upcoming tax payments, you can free up other cash.

Monday, March 31, 2014

7 Smart Ways to Take Advantage of Your Tax Refund

Sunday, March 30, 2014

Are the Earnings at Team Hiding Something?

It takes money to make money. Most investors know that, but with business media so focused on the "how much," very few investors bother to ask, "How fast?"

When judging a company's prospects, how quickly it turns cash outflows into cash inflows can be just as important as how much profit it's booking in the accounting fantasy world we call "earnings." This is one of the first metrics I check when I'm hunting for the market's best stocks. Today, we'll see how it applies to Team (NYSE: TISI ) .

Let's break this down

In this series, we measure how swiftly a company turns cash into goods or services and back into cash. We'll use a quick, relatively foolproof tool known as the cash conversion cycle, or CCC for short.

Why does the CCC matter? The less time it takes a firm to convert outgoing cash into incoming cash, the more powerful and flexible its profit engine is. The less money tied up in inventory and accounts receivable, the more available to grow the company, pay investors, or both.

To calculate the cash conversion cycle, add days inventory outstanding to days sales outstanding, then subtract days payable outstanding. Like golf, the lower your score here, the better. The CCC figure for Team for the trailing 12 months is 81.8.

For younger, fast-growth companies, the CCC can give you valuable insight into the sustainability of that growth. A company that's taking longer to make cash may need to tap financing to keep its momentum. For older, mature companies, the CCC can tell you how well the company is managed. Firms that begin to lose control of the CCC may be losing their clout with their suppliers (who might be demanding stricter payment terms) and customers (who might be demanding more generous terms). This can sometimes be an important signal of future distress -- one most investors are likely to miss.

In this series, I'm most interested in comparing a company's CCC to its prior performance. Here's where I believe all investors need to become trend-watchers. Sure, there may be legitimate reasons for an increase in the CCC, but all things being equal, I want to see this number stay steady or move downward over time.

Source: S&P Capital IQ. Dollar amounts in millions. FY = fiscal year. TTM = trailing 12 months.

Because of the seasonality in some businesses, the CCC for the TTM period may not be strictly comparable to the fiscal-year periods shown in the chart. Even the steadiest-looking businesses on an annual basis will experience some quarterly fluctuations in the CCC. To get an understanding of the usual ebb and flow at Team, consult the quarterly-period chart below.

Source: S&P Capital IQ. Dollar amounts in millions. FQ = fiscal quarter.

On a 12-month basis, the trend at Team looks good. At 81.8 days, it is 6.2 days better than the five-year average of 88. days. The biggest contributor to that improvement was DSO, which improved 12.4 days compared to the five-year average. That was partially offset by a 7.2-day increase in DPO.

Considering the numbers on a quarterly basis, the CCC trend at Team looks OK. At 107.6 days, it is 19.3 days worse than the average of the past eight quarters. Investors will want to keep an eye on this for the future to make sure it doesn't stray too far in the wrong direction. With quarterly CCC doing worse than average and the latest 12-month CCC coming in better, Team gets a mixed review in this cash-conversion checkup.

Though the CCC can take a little work to calculate, it's definitely worth watching every quarter. You'll be better informed about potential problems, and you'll improve your odds of finding underappreciated home run stocks.

Looking for alternatives to Team? It takes more than great companies to build a fortune for the future. Learn the basic financial habits of millionaires next door and get focused stock ideas in our free report, "3 Stocks That Will Help You Retire Rich." Click here for instant access to this free report.

Add Team to My Watchlist.A Few Things to Watch in the Commodities Market This Week...

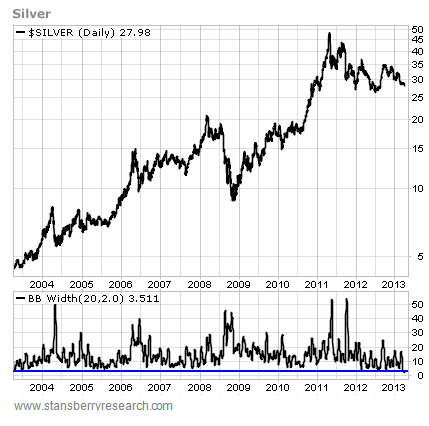

Bollinger Bands measure volatility. As you can see from the bottom chart – which measures BB width over the past 10 years – periods of low volatility are always followed by periods of high volatility, and vice versa. There's no way to know for sure which direction the move will go. But with silver now showing its lowest volatility in a decade, traders should get ready for a big move soon.

Bollinger Bands measure volatility. As you can see from the bottom chart – which measures BB width over the past 10 years – periods of low volatility are always followed by periods of high volatility, and vice versa. There's no way to know for sure which direction the move will go. But with silver now showing its lowest volatility in a decade, traders should get ready for a big move soon.  The MACD indicator helps to measure the strength of a trend. If the chart is moving higher and the MACD is moving higher as well, the rally is strong and likely to continue. In this case, though, the dollar has been rallying... but the MACD hasn't been keeping up. This negative divergence is an early warning sign the rally may be coming to an end.

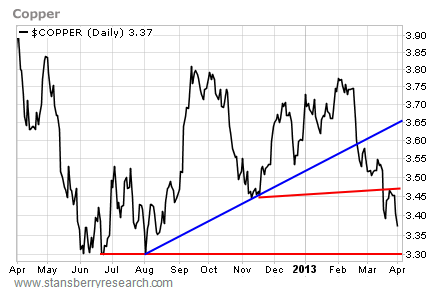

The MACD indicator helps to measure the strength of a trend. If the chart is moving higher and the MACD is moving higher as well, the rally is strong and likely to continue. In this case, though, the dollar has been rallying... but the MACD hasn't been keeping up. This negative divergence is an early warning sign the rally may be coming to an end.  Copper is a leading indicator for stock prices. The S&P 500 has managed to rally to new all-time highs, despite the drop in copper. But this sort of divergence usually doesn't last long. At some point, copper either needs to start rallying and catch up with the move in the stock market... or the stock market needs to fall in line with the move in copper. Best regards and good trading, Jeff Clark

Copper is a leading indicator for stock prices. The S&P 500 has managed to rally to new all-time highs, despite the drop in copper. But this sort of divergence usually doesn't last long. At some point, copper either needs to start rallying and catch up with the move in the stock market... or the stock market needs to fall in line with the move in copper. Best regards and good trading, Jeff Clark Saturday, March 29, 2014

6 Ways to Freshen Up Your Finances

Alamy Spring has arrived, and so has the inevitable seasonal cleaning duties. In addition to packing away the winter clothes, washing windows and cleaning out the fridge, spring is the perfect time to evaluate your financial situation and tidy up your budget, bank accounts, debts and investments. Here are six ways to spruce up your finances: 1. Refresh your budget. If you've been promoted, transitioned from two incomes to one or are starting a family, this is the perfect time to revisit your household budget. Consider using online personal finance tools to help you set a budget and keep track of your accounts. You'll see where your money is going and can adjust spending where needed to help you attain your financial goals. 2. Pay off holiday debt once and for all. Clear up your credit lines, and pay off the purchases you made over the holiday season. Put yourself on a stricter debt payoff plan specifically to pay off the debt you accumulated over the holidays. Cleaning up this debt quickly will put you in a much better financial position for the rest of the year. It's easy to fall back in to debt, so put a plan in place while you're at it to maintain a zero balance. 3. De-clutter your countertops and go paperless. A good way to cut down on clutter is to opt for electronic bill payments. It decreases the amount of print mail and can even help prevent identity theft. Secure your online bill payment with strong passwords that you change on a regular basis. Signing up for a vendor's online automatic pay system (helpful for fixed-payment bills such as cable and Internet) allows you to set up payments as "recurring" so the bills are automatically paid. This can help you avoid forgetting to pay a bill, and it keeps countertops paper-free. 4. Clean up your credit score. Boosting your credit score is always important, but before you do, it's imperative to learn about your credit history and the various accounts that affect it. To make sure your credit report is free of errors, get a free credit report (you're entitled to one free copy from the three credit bureaus every year). Check for any errors or accounts listed that aren't yours. Companies do make mistakes, and it's your responsibility to make corrections when you catch them, so your credit score isn't accidentally lowered. 5. Set up an emergency fund. Life is full of unexpected surprises. A car repair, illness or unemployment can catch you and your family off guard and leave you financially stranded. When the unexpected happens, it's important to have a stash of cash set aside in an emergency fund. At a minimum, it should hold three months worth of your living expenses. If you pay $2,000 a month to cover the basics such as housing, utilities and food, then put aside $6,000 in your emergency fund. If you have dependents, your emergency fund should consist of six months of your living expenses. 6. Dust off your financial statements. Review your bank and credit card statements as well as bills to make sure you're not being charged fees you don't recognize or paying for subscriptions or services you never use. This is also a great time to look at your insurance policies. Some personal finance tools expose fees that are often hidden on statements or buried in the fine print to help you eliminate unnecessary fees and save more money. Whether it's putting money aside to pay down debt, planning for the future or just getting organized, the changing season is a great time to change up your financial habits.

Alamy Spring has arrived, and so has the inevitable seasonal cleaning duties. In addition to packing away the winter clothes, washing windows and cleaning out the fridge, spring is the perfect time to evaluate your financial situation and tidy up your budget, bank accounts, debts and investments. Here are six ways to spruce up your finances: 1. Refresh your budget. If you've been promoted, transitioned from two incomes to one or are starting a family, this is the perfect time to revisit your household budget. Consider using online personal finance tools to help you set a budget and keep track of your accounts. You'll see where your money is going and can adjust spending where needed to help you attain your financial goals. 2. Pay off holiday debt once and for all. Clear up your credit lines, and pay off the purchases you made over the holiday season. Put yourself on a stricter debt payoff plan specifically to pay off the debt you accumulated over the holidays. Cleaning up this debt quickly will put you in a much better financial position for the rest of the year. It's easy to fall back in to debt, so put a plan in place while you're at it to maintain a zero balance. 3. De-clutter your countertops and go paperless. A good way to cut down on clutter is to opt for electronic bill payments. It decreases the amount of print mail and can even help prevent identity theft. Secure your online bill payment with strong passwords that you change on a regular basis. Signing up for a vendor's online automatic pay system (helpful for fixed-payment bills such as cable and Internet) allows you to set up payments as "recurring" so the bills are automatically paid. This can help you avoid forgetting to pay a bill, and it keeps countertops paper-free. 4. Clean up your credit score. Boosting your credit score is always important, but before you do, it's imperative to learn about your credit history and the various accounts that affect it. To make sure your credit report is free of errors, get a free credit report (you're entitled to one free copy from the three credit bureaus every year). Check for any errors or accounts listed that aren't yours. Companies do make mistakes, and it's your responsibility to make corrections when you catch them, so your credit score isn't accidentally lowered. 5. Set up an emergency fund. Life is full of unexpected surprises. A car repair, illness or unemployment can catch you and your family off guard and leave you financially stranded. When the unexpected happens, it's important to have a stash of cash set aside in an emergency fund. At a minimum, it should hold three months worth of your living expenses. If you pay $2,000 a month to cover the basics such as housing, utilities and food, then put aside $6,000 in your emergency fund. If you have dependents, your emergency fund should consist of six months of your living expenses. 6. Dust off your financial statements. Review your bank and credit card statements as well as bills to make sure you're not being charged fees you don't recognize or paying for subscriptions or services you never use. This is also a great time to look at your insurance policies. Some personal finance tools expose fees that are often hidden on statements or buried in the fine print to help you eliminate unnecessary fees and save more money. Whether it's putting money aside to pay down debt, planning for the future or just getting organized, the changing season is a great time to change up your financial habits.

Ford CEO gets 11% raise to $23.2M in 2013

The CEO earned a salary of $2 million and another $5.9 million in cash bonus as well as $15.3 million in long-term stock options, performance equity awards and compensation for items such as security and travel, according to a filing today with the U.S. Securities and Exchange Commission.

Mulally's salary remained unchanged from the previous year but his bonus grew. On the performance side, higher profits, cash flow and quality, under the Ford incentive formula, generated an additional $2 million for him because the company as a whole exceeded its targets.

Despite a fall in market share, Ford achieved 112% of its goals in 2013 compared with achieving only 75% of its goals in 2012 when quality scores fell.

The board also gave their CEO an incremental bonus of $2 million, which is allowed when the company has a stellar year in terms of performance and meeting overall objectives.

He also owns 6.2 million shares as of March 1.

Last year Mulally oversaw a company that earned almost $7.2 billion last year with record profits in North America, aggressive growth in Asia and restructuring in Europe and South America.

Mulally also remained at the helm after a period of speculation that he might leave to run Microsoft. He has said he will remain with Ford through the end of this year.

Since joining Ford in 2006, Mulally has made an "unbelievably profound impact on Ford," said David Cole, chairman emeritus of the Center for Automotive Research.

"If you paid him a billion dollars it would still be worth it. He changed the culture and led a transformation," Cole said.

Among other top executives:

■ Bill Ford, executive chairman, reported total compensation of $12 million including a $2 million salary.

■ Mark Fields, chief operating officer, received $10.1 million including a salary of $1.5 mi! llion.

■ Joe Hinrichs, president of The Americas, received $4.4 million including his $854,000 salary.

■ Bob Shanks, chief financial officer, had total compensation of $4 million with a $772,000 salary.

The annual meeting is set for May 8 where shareholders will vote on six proposals.

Contact Alisa Priddle at apriddle@freepress.com. Follow her on Twitter @AlisaPriddle

Friday, March 28, 2014

OptionsHouse Strategist Steve Claussen Explains Options Strategies

OptionsHouse's Chief Investment Strategist Steve Claussen dropped by for a chat on the Benzinga PreMarket Prep show on Wednesday, March 26. Claussen is always eager to share his knowledge of the market that is backed up by his career spanning over 25 years.

When asked if a retail investor should be investing in options instead of equities, Claussen first cautioned that with any investment, rule number one is not to invest with funds that an investor can't afford to lose.

So with that emphasized, is equities the best choice available to investors?

“That might be the case,” said Claussen. “You might say, hey, Microsoft (NASDAQ: MSFT), good stock. Not going anywhere, I'm going to buy $10,000 worth of stocks. And that's OK, they pay a decent dividend.”

Related: Axiom Capital's Gordon Johnson Discusses Solar Stocks, U.S. Steel

However, an investor completing this transaction has essentially concentrated exposure to one stock, which is what Claussen calls a “concentration risk.” If an investor is exposed too much to one holding, they run the risk of not being able to maximize their return and outperform the major indices.

This is where options comes in.

“Options can allow a $10,000 portfolio to spread that around five different companies, or five different ETFs, or five geographical ETFs,” Claussen argued. He added that an investor who holds an option at the end of the day has the right, but not the obligation, to own the stock. This strategy is best utilized by investors who at the end of the day may have an objective of owning the stock at some point in the future.

As is the case with any investment, options do come with risk.

An options holder in theory can see a 100 percent loss to their position.

“In options, one of the main advantages is you are spending less for the leverage you get versus buying the outright stock,” said Claussen.

Claussen is referring to the fact that options are leveraged, meaning an investor can stretch their money even further by buying options, which on a dollar-per-dollar basis is cheaper. He offered an example to show how options offer leverage using a stock that he holds in his family portfolio, Disney (NYSE: DIS).

If an investor bought 100 shares at $80, it would cost $8,000. Alternatively, an investor could purchase a call option for $75 per share, thereby gaining the same exposure to any rise in Disney shares while paying less.

Naturally, it is important to consider that options, unlike stock, have an expiry date. Once an option expires, it no longer has any value.

Timing is critically important, according to Claussen. In the Disney example, an investor who purchases an $82.50 out of the money call option would need shares of Disney to trade above $82.50 (known as the ‘strike price') mark to earn a profit.

Many novice investors would foolishly invest in and out of the money option chain only to see their investment lose value as shares fail to rise above the strike price.

Claussen's advice to new options trader is to create an options position that acts very much like a stock and its movement is more predictable. This is typically done by buying an in-the-money call option has both an intrinsic and extrinsic value.

Intrinsic value refers to the difference between the stock's price and the option's strike price. As an example, if a call options strike price is $15 and the stock is trading at $20, the intrinsic value of the call option is $5.

Related: Kor Group Founders Christopher Nagy & Dave Lauer Talk Market Structure, High Frequency Trading

Extrinsic value is the amount that an option's price is greater than the intrinsic value. This value declines as the expiration date draws closer.

“Out of the money options are 100 percent extrinsic value, they are a 100 percent wasting asset. In the money options, the portion that is in the money is not a wasting asset,” Claussen argued.

A popular strategy that investors are utilizing would be replacing their stock holdings with an option that has a delta of 0.7. A delta of 0.7 implies for every $1 the stock increases, the call options will increase by $0.70. If the stock continues to appreciate, the delta on the option will increase. By doing so, an investor is making less money as they would with owning the stock, but the investor has minimized his total liabilities by purchasing options for a cheaper price.

What if an investor doesn't want to sell their stock, but incorporate options to protect a profitable position or limit downside?

According to Claussen, an investor could keep their long position and reduce their exposure by selling a call option to collect a premium. Claussen gave a hypothetical example of selling an out-of-the-money (OTM) call option at a price that the stock may not reach. In the event that the stock in fact does not reach this price point, the investor keeps the entire premium received.

Selling an option involves substantial risk and should only be performed by sophisticated investors. Less sophisticated investors could consider buying a put option, which locks in a buying price for the investor to sell their stock at in the future.

Posted-In: disney Microsoft options Optionshouse PreMarket Prep Steve ClaussenNews Options Markets Interview Best of Benzinga

© 2014 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Most Popular UPDATE: BofA Announces $4B Buyback Plan, Raises Qtr. Dividend from $0.01 to $0.05/Share UPDATE: Facebook to Acquire Oculus VR for About $2B Advanced Cannabis Solutions Temporarily Gets CANN-ed Federal Reserve Board announces approval of capital plans of 25 bank holding companies participating in the Comprehensive Capital Analysis and Review Spotify Vs. Pandora Vs. Google Music Vs. iTunes Radio Vs. Xbox Music UPDATE: Bank of America Announces Settlements With Federal Housing Finance Agency (FHFA) and New York Attorney General Related Articles (MSFT + DIS) OptionsHouse Strategist Steve Claussen Explains Options Strategies Bank of America Says Structural Issues Could Pressure Microsoft's EPS Next 2-3 Years Microsoft Announces Expansion of Cloud Services for Mobile Scenarios ETFs Shrugging Off The Selling (DHS, SMH, IGF, INTC) GameStop Misses on Q4 Earnings - Analyst Blog Buying Into Oversold ETFs (BJK, SOCL, PBS, FB, GOOG) Around the Web, We're Loving...Thursday, March 27, 2014

Biotech funds: Only for those immune to fear

Our constant fear of diseases – stoked by ads for drugs to combat illness – may be one reason behind the boom in biotechnology stocks. More likely, however, is our fondness for a good story and a red-hot stock. Biotech has been so hot the past two years that the sector is starting to raise red flags. And, while it may have longer to run, it's an area that the weak of heart and the short of cash should avoid.

Despite a recent backup – more on that in a moment – biotech funds are standouts in an otherwise mediocre quarter for mutual fund investors. The average health and biotech fund has gained 5.4% this year vs. 0.2% for the average stock fund. The difference is more striking if you look at the funds' three-year records: They're up 100% vs. 46% for the average stock fund.

Those big gains have raised the question of whether biotech is in a bubble, which is in itself a loaded question. By definition, bubbles are extraordinarily difficult to detect before they pop. And high returns are not, by themselves, the only hallmark of a bubble. CBS is up 1,902% since the stock market bottom in 2009, but no one is claiming that media stocks are in a bubble.

What makes bubbles so hard to spot? For one thing, there's always a plausible story behind them. In the 1830s, canal stocks boomed because it is indeed much easier to push something over water than over rutted dirt roads. And in the 1990s, people invested in the dot-com bubble because they believed that the Internet would be an enormous gateway for commerce – which, in fact, it has evolved to be.

With biotechnology, the plausible story is that medicine is making some spectacu! lar breakthroughs, and doing so after a fairly long dry spell. The most notable is Gilead Sciences' hepatitis C drug Sovaldi, which actually cures the disease rather than controls it. The disease makes life a misery for 150 million to 200 million people around the world and ultimately kills many of them.

"Biotechnology is a real, great American story," says Rajiv Kaul, portfolio manager of Fidelity's Select Biotechnology Portfolio (FBIOX). "It's very difficult to make medicine. It takes hard work and the failure rates are high. But it's a really exciting time."

Furthermore, the industry's rise has come after a fairly long dry spell, when relatively few blockbuster drugs hit the market, says Evan McCulloch, portfolio manager of Franklin Biotechnology Discovery Fund. "Big pharma and biotech together had a significant period of underperformance," McCulloch says. During that period, biotech became extremely cheap relative to earnings.

Another problem in the middle part of the last decade: The Food and Drug Administration became more conservative after the failure of Vioxx, an anti-inflammatory drug sold by Merck, was shown to increase the risk of stroke and heart failure in patients. Currently, however, the FDA has been more accommodative toward getting new drugs on the market, says Kaul. "The FDA is doing the right things, and government has done good things in terms of working with industry to get innovative therapies to be priorities," he says.

The question then is whether investors are getting too giddy about the prospects for biotech stocks. Gilead (GILD), for example, sells for about 12.4 times its estimated 12 months' earnings, which is fairly reasonable. On the other end of the spectrum is Intercept Pharmaceuticals (ICPT), up 748% the past 12 months with no earnings.

But the market for small-company biotech stocks has always been giddy. One way to look at frothiness is the number of initial public offerings in the biotech industry – 25 in the industry this year alone! vs. 45 l! ast year. In a biotech bubble, you start seeing IPOs of companies composed of two guys, a microscope, and a dream. "It's not that bad yet," McCulloch says. "Companies raise money when they can, not necessarily when they need it." And right now is an excellent time for most companies to raise IPO money.

Nevertheless, biotech is a sector that has had a good run, which means that investors are likely to become skittish quickly. In the past few weeks, biotech stocks have sold off, in part because of Rep. Henry Waxman's recent letter to Gilead questioning the company's $84,000 price tag for Sovaldi. "It was a shot across the bow," says McCulloch. "And what it means is that there could be some revision to drug pricing in the long term."

Any laws restricting drug pricing are highly unlikely in the Republican-held House, however, and Gilead's champions note that the drug's price tag is far less than for a liver transplant or for the years of care needed by hepatitis C sufferers. But the letter may make companies wary of their pricing – not necessarily a bad thing. "Companies want their prices as high as they can make them without landing on front page of newspaper," McCulloch says.

Right now, it's hard to recommend biotech investing for anyone but those who don't mind risk. While the best years of biotech may be before us – and they probably are – you don't want to pay too much for the future. For the brave, the top-performing health and biotech companies are in the chart. Otherwise, consider a general diversified fund. Health care is about 13% of the Standard and Poor's 500 stock index. You don't want your portfolio to come down with unwanted side effects, such as itching, sneezing or hives.

A Cautious, Reluctant Bull

I hesitate to claim that Newton's Law—A body in motion will continue in motion, unless acted upon by an outside force—applies to the stock market; yet, in almost all our studies of past bear markets or crashes, there were causal factors that triggered the downturn, suggests Jim Stack in InvesTech Market Analyst.

Over the past 50 years, the most common trigger was a reversal or tightening in monetary policy. If you overlay a long-term graph of the 90-day T-bill yield, with the S&P 500 (SPX), this relationship becomes clearly visible.

One of the problems, however, is the variability in tightening, or interest rate increases, before trouble started in the stock market. Thus, the reason for watching as many reliable warning flags as possible.

It's only natural that the size of last year's gain would make one more nervous about the prospects for 2014. However, statistically speaking, the bearish odds did not increase simply because last year was a great year in the market.

Since 1928, there have been 18 years in which the S&P 500 increased over 25% (including 2013). Almost two-thirds of the subsequent years (61%) saw the market continue to rise the following year, with over twice as many double-digit gains as double-digit losses.

That doesn't imply we should expect double-digit gains this year, yet it allows us to remain cautiously optimistic in the absence of bearish evidence.

In addition, breadth rebounded so sharply last month that it registered not one, but two new "breadth thrusts." A "breadth thrust" takes place when the ten-day total of advancing stocks outpaces declining stocks by a wide margin.

This kind of upward momentum is often seen near the beginning of a new bull market or at the start of a new bull market leg upward.

We found that, since 1950, there have been only four instances when the S&P 500 was down more than 4% six months after a thrust was first observed. Also, there was only one double-digit loss (-10%), which occurred during the 1973-74 bear market.

So, bottom line, we are encouraged about this bull market's prospects over the balance of this year. With the margin debt and small-cap excesses described inside, I'm reluctant to speculate how long this bull market will last.

However, I don't mind being a "cautious, reluctant bull," as long as we're prepared to quickly adjust our allocation level downward, if warning flags start to increase.

Subscribe to InvesTech Market Analyst here…

More from MoneyShow.com:

A Rare "Zweig" Buy Signal

What's Next for Gold Stocks?

Corrections: Historical Observations

Darden Restaurants: Breakup Battle Heats Up

The gloves are off. Barington Capital Group, which first proposed restructuring Darden Restaurants (DRI) by working with management, has changed course and asked Darden's independent directors to name an independent chairman and consider hiring a new CEO.

Bloomberg

Bloomberg Barington, which previously reported that it controlled more than 2% of Darden shares, also announced its support of Starboard Value's push to allow shareholders to vote on the company's proposed Red Lobster separation. See the details in this morning's press release.

The news comes in the wake of a number of moves by Darden that could be seen as less than shareholder friendly. Earlier this month the company replaced its investor day meeting with individual meetings with shareholders and analysts. Then last week Darden amended its corporate bylaws. The company's SEC filing said the amendments were made as part of its regular corporate governance review and the bylaws were updated to address current market practices.

The amendments require shareholders proposing director nominations or additional business at a shareholder meeting to hold their shares through the date of the meeting. They also have to make additional disclosures regarding their interest in the company, the business being proposed and/or their relationship with the shareholder nominees. Those being nominated for director must also make additional disclosures.

"As we have said previously, our focus is on doing what is in the best interest of all Darden shareholders and the Board is confident in the actions the Company is taking to deliver on this responsibility," the company said in an email. "We have been speaking directly with our shareholders and look forward to continuing that dialogue."

ISS Corporate Services has given Darden's corporate governance a QuickScore of 10 out of a range of 1 (low governance risk) to 10 (high governance risk). ISS highlights fact that the chairman and CEO roles have not been separated that and that 45% of the non-executive board members have lengthy tenure.

Darden shares rose slightly on the Barington news. They’re up 0.3% to $50.86 at 2:09 p.m. today, as by now it's likely a far gone conclusion that the battle over Darden's future is likely to be heated.

Wednesday, March 26, 2014

InterCloud Systems (ICLD) Stock Continues To Decline In Aftermarket Trading

NEW YORK (TheStreet) -- Intercloud Systems Inc. (ICLD) shares were down 2.4% to $7.20 in aftermarket trading Wednesday, following a precipitous drop for the telecom infrastructure company throughout the day.

The stock closed down 7.5% during the day after three separate law firms sent out press releases stating that they were filing lawsuits against the company on behalf of shareholders. Levi & Korinsky, LLP's lawsuit alleges that InterCloud "made materially false and misleading statements and/or omitted materially adverse facts regarding the company's business, operations, and prospects."

According to the complaints, InterCloud hired a promotional firm, The Dream Team Group (DTG), to promote the stock after the company's IPO. "DTG, along with its affiliates and other third parties, published articles touting the company's stock without disclosing that they were paid promoters for the company, a violation of Section 17(b) of the Securities Act of 1933," law firm Rigrodsky & Long, PA said.

Must Read: Warren Buffett's 10 Favorite Stocks

STOCKS TO BUY: TheStreet Quant Ratings has identified a handful of stocks that can potentially TRIPLE in the next 12 months. Learn more.

Stock quotes in this article: ICLDNissan recalls 1 million vehicles due to airbag flaw

Timeline: What went wrong at GM NEW YORK (CNNMoney) Nissan Motor is recalling more than 1 million vehicles in the United States and Canada to fix a software problem that could prevent the front passenger airbag from deploying in an accident.

Timeline: What went wrong at GM NEW YORK (CNNMoney) Nissan Motor is recalling more than 1 million vehicles in the United States and Canada to fix a software problem that could prevent the front passenger airbag from deploying in an accident. Nissan (NSANF) said it is not aware of any deaths caused by the problem, but can not give details about resulting injuries.

The problem is with the sensors in the front passenger seats that are supposed to tell if an adult or a child is sitting on the seat. Because the risk of injury or death to child is greater from an airbag than from an accident itself, if the system senses there is not enough weight in the front passenger seats, that airbag will not deploy.

The problem with the Nissans is that the sensors are shutting off the airbag even if an adult is in the seat.

The cars being recalled are most of the best-selling Nissan and luxury Infiniti models from the last two years. They include the 2013-2014 Altima, Leaf, Pathfinder and Sentra, the model year 2013 NV200 cargo van that's also known as the Nissan taxi, the 2013 Infiniti JX35, and the 2014 Infiniti Q50 and QX60 cars.

Inside Nissan's 'Taxi of Tomorrow'

Inside Nissan's 'Taxi of Tomorrow' The recall comes as the industry and safety regulators at the National Highway Traffic Safety Administration are focused on a recall of 1.6 million vehicles worldwide by General Motors (GM, Fortune 500). A problem with the ignition system can cause the car to shut off while driving, disabling not only the airbags but also the power steering and brakes.

At least 12 deaths have been caused by GM's ignition defect. GM has come under harsh criticism, and CEO Mary Barra has made numerous apologies, due to revelations that its engineers were aware of the problem as early as 2004 but did not order a recall until February of this year.

The GM ignition switch is not the only large auto industry recall getting attention in recent months. Honda (HMC) has recalled 900,000 Odyssey minivans due to fire risk, and GM announced another round of recalls covering 1.5 million U.S. cars. Toyota Motor (TM) agreed to pay a $1.2 billion fine to settle a criminal probe into its co! nduct surrounding a 2010 recall for unintended acceleration. ![]()

Tuesday, March 25, 2014

3 Stock Spinoffs That Will Outperform Their Parents

Popular Posts: 5 Blue-Chip Stocks Set to Boom Even MoreThe Best Ways to Buy the Alibaba IPOAmerican Funds: 5 Mutual Funds to Buy Recent Posts: 3 Homebuilders Building on Solid Foundations 3 Stock Spinoffs That Will Outperform Their Parents Take Buffett’s Advice: 5 Vanguard Funds to Buy View All Posts

Popular Posts: 5 Blue-Chip Stocks Set to Boom Even MoreThe Best Ways to Buy the Alibaba IPOAmerican Funds: 5 Mutual Funds to Buy Recent Posts: 3 Homebuilders Building on Solid Foundations 3 Stock Spinoffs That Will Outperform Their Parents Take Buffett’s Advice: 5 Vanguard Funds to Buy View All Posts

Spinoffs — they’re hot right now.

Companies from all kinds of industries are divesting subsidiaries that don't fit by spinning them out into independent, separately run businesses. Generally, spinoffs outperform the S&P 500 in their first 12 months of trading, making them very attractive to investors. Especially interested are existing shareholders of the parent company. They're wondering whether they should sell the new shares they receive, keep them, or sell their shares in the parent and reinvest the proceeds in the new company.

It's not a slam-dunk decision.

Let me make it a little easier. Here are my three choices of spinoffs that will outperform their parent over the next 12 to 18 months.

Top Spinoffs: Lands’ End InvestorPlace contributor James Brumley believes Eddie Lampert's move to spin off Lands' End from its parent – Sears Holdings (SHLD) — is simply a $500 million lifeline. While I agree the dividend is burdensome, it isn't life-threatening. The interest expense in 2014 on the $515 credit facility used to pay the dividend is estimated to be $25 million. Lands' End's operating income in 2012 was $82 million; in the first three quarters of fiscal 2013 it's 35% higher year-over-year. It will be fine.

InvestorPlace contributor James Brumley believes Eddie Lampert's move to spin off Lands' End from its parent – Sears Holdings (SHLD) — is simply a $500 million lifeline. While I agree the dividend is burdensome, it isn't life-threatening. The interest expense in 2014 on the $515 credit facility used to pay the dividend is estimated to be $25 million. Lands' End's operating income in 2012 was $82 million; in the first three quarters of fiscal 2013 it's 35% higher year-over-year. It will be fine.

Before making any investment it's smart to assess the business and its financial underpinnings. In that regard Lands' End doesn't fare too badly. The company's operating profits have been in decline in recent years, falling from $194 million in fiscal 2010 to $82 million in fiscal 2012. However, that's likely to bounce back in fiscal 2013, coming in somewhere north of $100 million.

Its direct segment, which includes internet and catalog sales and represents 82% of its overall revenue, is highly profitable. For the first 39 weeks of fiscal 2013 ended Nov. 1, the direct segment's revenue was $861 million with operating profits of $76 million. Revenues and operating income grew 1% and 9.6% year-over-year respectively. More important, its operating margins grew 80 basis points to 8.8%. It's the heart of the business.

The fly in the ointment is its retail segment, which had an operating loss of $4.5 million on $172 million in revenue. Its retail business consists of 275 Lands' End Shops at Sears and 16 stand-alone Lands' End Inlet stores. When you consider this revenue was generated from 2.2 million square feet (a dismal average of $80 per square foot), it's not hard to understand why it lost money. Lands' End's No. 1 priority as an independent company is to improve the sales productivity at its Sears locations. If it can double the sales per square foot to $160, you can be sure the segment will be profitable.

Regardless of the retail segment's troubles, I believe SHLD shareholders should sell some or all of their shares once Lands' End is spun off, using the proceeds to buy more. Spinoffs usually outperform. This one will do so by a country mile.

Top Spinoffs: Gaming and Leisure Properties Although Penn National Gaming (PENN) completed the spinoff of its real estate assets on Nov. 1, 2013, Gaming and Leisure Properties' (GLPI) shares have traded since mid-October. The only pure-play Casino REIT was created to provide PENN shareholders with two investments: gaming and real estate. Both businesses would be able to focus on what they do best with shareholders better off as a result. I can't argue with the rationale.

Although Penn National Gaming (PENN) completed the spinoff of its real estate assets on Nov. 1, 2013, Gaming and Leisure Properties' (GLPI) shares have traded since mid-October. The only pure-play Casino REIT was created to provide PENN shareholders with two investments: gaming and real estate. Both businesses would be able to focus on what they do best with shareholders better off as a result. I can't argue with the rationale.

PENN shareholders received one share of GLPI for every share of the gaming operation. In order to qualify as a REIT, GLPI was required to purge itself of all accumulated earnings. It did so by paying $210 million in cash and 22 million shares to existing shareholders. The special dividend amounted to $11.84 per share, or $1.05 billion. Even though this is a great gift for the shareholders of record and many have likely sold their GLPI shares, I believe the best is yet to come.

Think about the state of U.S. gambling at the moment. Although Las Vegas and the rest of the gambling hot spots across the country are slowly pulling themselves off the mat, we all know the real money right know is in Asia and other parts of the world. All you have to do is look at the share price of Las Vegas Sands (LVS) to know that the Macau operators are the ones winning at the moment. At some point the U.S. will bounce back as more states accept the reality that some tax revenue from gambling is better than none.

For all we know, PENN will be the winner when it comes to the domestic gambling scene. Then again, maybe it won't. GLPI's announced in December that it was buying the real estate assets of the Casino Queen in East St. Louis for $140 million — the first indication of how it intends to grow its business. Up until then all of 19 casino facilities were formerly owned by PENN, with 17 still operated by them. The Casino Queen deal screams, "We don't know who's going to win on the U.S. gaming front so we want to own as many of the potential winners as possible." If you bet on PENN and it doesn't do so well, its stock goes down. GLPI, on the other hand, continues to collect the rent. The cash flow continues whether or not Penn is operating the casino.

You can bet on Penn — or you can sell PENN, hang on to your GLPI stock and buy LVS stock with the PENN proceeds. That to me seems like a much smarter bet. But I'm no gambler.

Top Spinoffs: Ashford Hospitality Prime It seems there are two price points that win in this world: high and low. Ashford Hospitality Trust (AHT) came to the conclusion that its revenue per available room (RevPAR) of $102 was primarily from middle-of-the-road hotels. Nice, but generally inexpensive. The eight hotels it rolled into Ashford Hospitality Prime (AHP) are of a higher price point, averaging a RevPAR of $145 — double the national average. Investors would easily see the difference between the two portfolios, making both stocks more attractive.

It seems there are two price points that win in this world: high and low. Ashford Hospitality Trust (AHT) came to the conclusion that its revenue per available room (RevPAR) of $102 was primarily from middle-of-the-road hotels. Nice, but generally inexpensive. The eight hotels it rolled into Ashford Hospitality Prime (AHP) are of a higher price point, averaging a RevPAR of $145 — double the national average. Investors would easily see the difference between the two portfolios, making both stocks more attractive.

Shareholders received one share of AHP stock for every five shares of AHT. Since AHP stock started trading on the NYSE (Nov. 20) it's down 26% through March 20. Meanwhile, AHT stock is up 33% in the same period. Clearly investors see the split as a good thing for the parent.

Long-term it should be good for both.

Since becoming a separately run, independent company, AHP has acquired two additional hotels — The Sofitel Chicago Water Tower and Pier House Resort and Spa — for $246 million. It paid $653,000 per room for the Pier House, which is located in Key West, Fla., the second-highest RevPAR in the U.S.. The Pier House was acquired from AHT while the Sofitel was purchased from an affiliate of Blackstone (BX). It has an option on 12 more hotels currently owned by AHT whose RevPAR skew higher. Long-term, AHP’s RevPAR is only going to go higher, setting it apart from the rest of the public lodging universe … including AHT.

In this particular example I'd recommend you hang on to both AHT and AHP stock because they address separate markets. You also might want to pick up more AHP given its decline since November. Long-term you'll be happy you did.

As of this writing, Will Ashworth did not own a position in any of the aforementioned securities.

Mid-Morning Market Update: Markets Open Higher; Tiffany Posts Downbeat Earnings

Related BZSUM #PreMarket Primer: Friday, March 21: US Expands Russian Sanctions Mid-Afternoon Market Update: Walter Energy Gets Pounded as Markets Rise

Related BZSUM #PreMarket Primer: Friday, March 21: US Expands Russian Sanctions Mid-Afternoon Market Update: Walter Energy Gets Pounded as Markets Rise Following the market opening Friday, the Dow traded up 0.44 percent to 16,402.68 while the NASDAQ surged 0.04 percent to 4,320.84. The S&P also rose, gaining 0.46 percent to 1,880.67.

Leading and Lagging Sectors

Friday morning, the utilities sector proved to be a source of strength for the market. Leading the sector was strength from Huaneng Power International (NYSE: HNP) and Exelon (NYSE: EXC). In trading on Friday, telecommunications services shares were relative laggards, down on the day by about 0.01 percent.

Among the sector stocks, 8x8 (NASDAQ: EGHT) was down more than 2.2 percent, while USA Mobility (NASDAQ: USMO) tumbled around 2.5 percent.

Top Headline

Tiffany & Co (NYSE: TIF) swung to a loss in the fourth quarter. Tiffany posted a quarterly loss of $103.6 million, or $0.81 per share, versus a year-ago profit of $179.6 million, or $1.42 per share. Excluding special items, it earned $1.47 per share. Its revenue climbed to $1.30 billion versus $1.24 billion. However, analysts were estimating earnings of $1.51 per share on revenue of $1.31 billion. For fiscal year 2014, Tiffany projects earnings of $4.05 to $4.15 per share, versus analysts' estimates of $4.27 per share.

Equities Trading UP

Endocyte (NASDAQ: ECYT) shares shot up 121.31 percent to $32.40 after Merck & Co (NYSE: MRK) and Endocyte announced the European CHMP positive opinions for VYNFINIT and the companion agents FOLCEPRI and NEOCEPRI.

Shares of LIN Media LLC (NYSE: LIN) got a boost, shooting up 30.67 percent to $28.08 after Media General (NYSE: MEG) announced its plans to buy Lin Media LLC for $1.6 billion.

CommScope Holding Company (NASDAQ: COMM) was also up, gaining 11.66 percent to $24.71 after the company lifted its Q1 forecast.

Equities Trading DOWN

Shares of Symantec (NASDAQ: SYMC) were down 11.70 percent to $18.46 after the company fired President and Chief Executive Steve Bennett and appointed director Michael Brown as interim president and CEO. UBS downgraded the stock from Buy to Neutral and lowered the price target from $27.00 to $21.00.

AAR (NYSE: AIR) shares tumbled 6.23 percent to $28.99 after the company reported a drop in its Q3 profit and lowered its FY14 forecast.

Nike (NYSE: NKE) was down, falling 3.89 percent to $76.19 after the company issued a cautious forecast for 2015 earnings. Nike posted its quarterly adjusted profit of $0.73 per share on revenue of $6.97 billion.

Commodities

In commodity news, oil traded up 0.27 percent to $99.17, while gold traded up 0.53 percent to $1,337.80.

Silver traded down 0.05 percent Friday to $20.42, while copper rose 1.52 percent to $2.97.

Eurozone

European shares were mostly higher today.

The Spanish Ibex Index fell 0.18 percent, while Italy's FTSE MIB Index rose 0.20 percent.

Meanwhile, the German DAX surged 0.19 percent and the French CAC 40 gained 0.01 percent while U.K. shares rose 0.10 percent.

Economics

On the economics calendar Friday, there is no important data due out.

Posted-In: Earnings News Guidance Eurozone Futures Forex Global Econ #s Economics Intraday Update Markets Movers Tech

© 2014 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Most Popular Are Massive Xbox One 'Titanfall' Sales To Blame For Xbox 360 Game Delay? BofA Releases Results from Annual Stress Test, Estimates Assume No Changes to Dividend Morgan Stanley Considers Possible Impact of Office on iPad for Microsoft All Star Charts' J.C. Parets On Why BlackBerry Shares Will Double Results of Fed Stress Test; March 20 2014 The 'Green Rush' Is Bringing Traders New And Old Into To The Fold Of Marijuana Stocks Related Articles (AIR + BZSUM) Mid-Morning Market Update: Markets Open Higher; Tiffany Posts Downbeat Earnings AAR Corp Lags Fiscal Q3 Earnings Ests - Analyst Blog #PreMarket Primer: Friday, March 21: US Expands Russian Sanctions Mid-Afternoon Market Update: Walter Energy Gets Pounded as Markets RiseMonday, March 24, 2014

3 Stock Spinoffs That Will Outperform Their Parents

Popular Posts: 5 Blue-Chip Stocks Set to Boom Even MoreThe Best Ways to Buy the Alibaba IPOAmerican Funds: 5 Mutual Funds to Buy Recent Posts: 3 Homebuilders Building on Solid Foundations 3 Stock Spinoffs That Will Outperform Their Parents Take Buffett’s Advice: 5 Vanguard Funds to Buy View All Posts

Spinoffs — they’re hot right now.

Companies from all kinds of industries are divesting subsidiaries that don't fit by spinning them out into independent, separately run businesses. Generally, spinoffs outperform the S&P 500 in their first 12 months of trading, making them very attractive to investors. Especially interested are existing shareholders of the parent company. They're wondering whether they should sell the new shares they receive, keep them, or sell their shares in the parent and reinvest the proceeds in the new company.

It's not a slam-dunk decision.

Let me make it a little easier. Here are my three choices of spinoffs that will outperform their parent over the next 12 to 18 months.

Top Spinoffs: Lands’ EndInvestorPlace contributor James Brumley believes Eddie Lampert's move to spin off Lands' End from its parent – Sears Holdings (SHLD) — is simply a $500 million lifeline. While I agree the dividend is burdensome, it isn't life-threatening. The interest expense in 2014 on the $515 credit facility used to pay the dividend is estimated to be $25 million. Lands' End's operating income in 2012 was $82 million; in the first three quarters of fiscal 2013 it's 35% higher year-over-year. It will be fine.

Before making any investment it's smart to assess the business and its financial underpinnings. In that regard Lands' End doesn't fare too badly. The company's operating profits have been in decline in recent years, falling from $194 million in fiscal 2010 to $82 million in fiscal 2012. However, that's likely to bounce back in fiscal 2013, coming in somewhere north of $100 million.

Its direct segment, which includes internet and catalog sales and represents 82% of its overall revenue, is highly profitable. For the first 39 weeks of fiscal 2013 ended Nov. 1, the direct segment's revenue was $861 million with operating profits of $76 million. Revenues and operating income grew 1% and 9.6% year-over-year respectively. More important, its operating margins grew 80 basis points to 8.8%. It's the heart of the business.

The fly in the ointment is its retail segment, which had an operating loss of $4.5 million on $172 million in revenue. Its retail business consists of 275 Lands' End Shops at Sears and 16 stand-alone Lands' End Inlet stores. When you consider this revenue was generated from 2.2 million square feet (a dismal average of $80 per square foot), it's not hard to understand why it lost money. Lands' End's No. 1 priority as an independent company is to improve the sales productivity at its Sears locations. If it can double the sales per square foot to $160, you can be sure the segment will be profitable.

Regardless of the retail segment's troubles, I believe SHLD shareholders should sell some or all of their shares once Lands' End is spun off, using the proceeds to buy more. Spinoffs usually outperform. This one will do so by a country mile.

Top Spinoffs: Gaming and Leisure PropertiesAlthough Penn National Gaming (PENN) completed the spinoff of its real estate assets on Nov. 1, 2013, Gaming and Leisure Properties' (GLPI) shares have traded since mid-October. The only pure-play Casino REIT was created to provide PENN shareholders with two investments: gaming and real estate. Both businesses would be able to focus on what they do best with shareholders better off as a result. I can't argue with the rationale.

PENN shareholders received one share of GLPI for every share of the gaming operation. In order to qualify as a REIT, GLPI was required to purge itself of all accumulated earnings. It did so by paying $210 million in cash and 22 million shares to existing shareholders. The special dividend amounted to $11.84 per share, or $1.05 billion. Even though this is a great gift for the shareholders of record and many have likely sold their GLPI shares, I believe the best is yet to come.

Think about the state of U.S. gambling at the moment. Although Las Vegas and the rest of the gambling hot spots across the country are slowly pulling themselves off the mat, we all know the real money right know is in Asia and other parts of the world. All you have to do is look at the share price of Las Vegas Sands (LVS) to know that the Macau operators are the ones winning at the moment. At some point the U.S. will bounce back as more states accept the reality that some tax revenue from gambling is better than none.

For all we know, PENN will be the winner when it comes to the domestic gambling scene. Then again, maybe it won't. GLPI's announced in December that it was buying the real estate assets of the Casino Queen in East St. Louis for $140 million — the first indication of how it intends to grow its business. Up until then all of 19 casino facilities were formerly owned by PENN, with 17 still operated by them. The Casino Queen deal screams, "We don't know who's going to win on the U.S. gaming front so we want to own as many of the potential winners as possible." If you bet on PENN and it doesn't do so well, its stock goes down. GLPI, on the other hand, continues to collect the rent. The cash flow continues whether or not Penn is operating the casino.

You can bet on Penn — or you can sell PENN, hang on to your GLPI stock and buy LVS stock with the PENN proceeds. That to me seems like a much smarter bet. But I'm no gambler.

Top Spinoffs: Ashford Hospitality PrimeIt seems there are two price points that win in this world: high and low. Ashford Hospitality Trust (AHT) came to the conclusion that its revenue per available room (RevPAR) of $102 was primarily from middle-of-the-road hotels. Nice, but generally inexpensive. The eight hotels it rolled into Ashford Hospitality Prime (AHP) are of a higher price point, averaging a RevPAR of $145 — double the national average. Investors would easily see the difference between the two portfolios, making both stocks more attractive.

Shareholders received one share of AHP stock for every five shares of AHT. Since AHP stock started trading on the NYSE (Nov. 20) it's down 26% through March 20. Meanwhile, AHT stock is up 33% in the same period. Clearly investors see the split as a good thing for the parent.

Long-term it should be good for both.

Since becoming a separately run, independent company, AHP has acquired two additional hotels — The Sofitel Chicago Water Tower and Pier House Resort and Spa — for $246 million. It paid $653,000 per room for the Pier House, which is located in Key West, Fla., the second-highest RevPAR in the U.S.. The Pier House was acquired from AHT while the Sofitel was purchased from an affiliate of Blackstone (BX). It has an option on 12 more hotels currently owned by AHT whose RevPAR skew higher. Long-term, AHP’s RevPAR is only going to go higher, setting it apart from the rest of the public lodging universe … including AHT.

In this particular example I'd recommend you hang on to both AHT and AHP stock because they address separate markets. You also might want to pick up more AHP given its decline since November. Long-term you'll be happy you did.

As of this writing, Will Ashworth did not own a position in any of the aforementioned securities.

Retirement Confidence Up for No Good Reason: EBRI

Confidence in retirement security is up, according to EBRI’s 24th annual Retirement Confidence Survey, but the organization was reluctant to declare victory. Although more Americans reported feeling confident in 2014 than in the last five years, EBRI did not find they’re more prepared.

The survey found 37% of Americans are at least somewhat confident about their ability to retire comfortably, with 18% saying they are very confident, up from 13% last year. However, the percentage who said they were not at all confident is statistically unchanged at nearly a quarter, according to the report.

On the bright side (and not very surprising), the survey found confidence is higher among those who participate in a retirement plan, either through their workplace or in an individual account.

“When we compare the shifts in confidence between the 2014 and 2013 surveys, the increase in confidence was almost exclusively among those with a retirement plan,” Jack VanDerhei, research director for EBRI, said on a call discussing the results on Tuesday.

However, savings are still low and few respondents reported taking basic steps to prepare for retirement. The survey found 35% of workers have not saved any money at all for retirement, and only 57% are actively saving.

“Beyond participation in a retirement plan, there appeared to be no significant behavioral change to account for the change in confidence,” VanDerhei said. “Indeed, many clear warning signs about Americans’ lack of preparation for retirement have not changed. In aggregate, workers were no more likely to have done a retirement needs calculation, to have saved for retirement or to report savings amounts significantly larger than that captured in 2013.”

Greg Burrows, senior vice president of retirement and investor services for The Principal, spoke about the survey results in an interview with ThinkAdvisor on Monday. He noted how important it is for workers to assess what their actual retirement needs will be, rather than just guessing.

“One thing we look at is the percentage of workers using calculators, and still only about 44% use them, which means over half are still guessing at what their needs are,” Burrows said. “Amongst our clients and participants, we find that those who use retirement calculators, 40% of them take positive action and on average they’re saving about 40% more.”

Almost half of workers without a retirement plan said they were not at all confident about their retirement prospects, compared with about one-tenth of people who do have a plan.

Not only are those without a plan worried about their retirement, they’re not showing any improvement. Among workers who have a retirement plan, those who reported feeling very confident nearly doubled from 14% in 2013 to 24% this year, while those without a plan dropped one point to 9%.

The bad news keeps piling up for workers who don’t have a retirement plan. EBRI found that almost three-quarters of those who say they or their spouse don’t have a plan have less than $1,000 in total assets saved.

Burrows noted that percentage of workers with such meager savings has increased over the past five years by more than 50%. “There’s a disconnect between an awareness of the need to save versus the action behind the saving itself,” he said. “We’d recommend people really concentrate on understanding their expenses so they can make saving part of their lifestyle and they can think about savings as a consumption item to incorporate in their planning process.”

The worst part is workers know they need to save more. More than 20% of workers said they needed to save at least 30% of their income. Almost a quarter of those without a retirement plan said they needed to save at least 50% or that they had no idea how much they should be saving.

EBRI credited the confidence boost to market improvements.

“One possible reason for the improved confidence is the rising stock market and property values, and to the extent that those factors carry forward to retirement savings account balances, there may be merit to that assessment,” VanDerhei said.

Mathew Greenwald, president of Mathew Greenwald & Associates, which conducted the survey for EBRI, agreed with the assessment that economic improvements drive investors’ optimism. “It appears that people make some assumptions about how financially secure they will be in the future based on how well the economy is performing now,” he said on the call. However, “with economic conditions being somewhat cyclical, this obviously is not a good way of making judgments or predictions about the future.”

There were the same familiar obstacles to saving—cost of living, day-to-day expenses—but the study found debt is another major impediment. Of workers who said debt was a major problem for them, just 3% said they are very confident about their ability to retire. By comparison, 29% of workers who said debt was not a problem reported feeling very confident.

Debt affects retirees, too. Forty-four percent of retirees said they were uncomfortable with their level of debt. Nearly 60% of workers agreed.

Burrows urged advisors to work with their clients on a budget to identify where they can cut back and address problems with debt.

“I can’t emphasize enough the importance of understanding the expense side of the ledger in order to put yourself in a position to save,” he said. “Saving’s not an easy thing. It’s not unlike a diet. When you start a diet you think about what you eat and monitoring what you do. With more information, people can be in a better position to make decisions that might be helpful to them. It really does start with some of the basics. We understand that the basics can be really hard, but they’re really important, especially over the long term.”

Another troubling finding in the 2014 survey is that current workers may rely too much on their chances of just working longer if they reach retirement age and don’t have enough. Two-thirds of workers said they plan to work for pay in retirement. However, only 27% of retirees said they do so.

“We seem to be in the midst of a redefinition of retirement,” Greenwald said. “The biggest shift we have seen in the 24 years we have conducted the Retirement Confidence Survey is the movement of workers toward planning to work later in life.”

Greenwald noted that in 1991, 84% of workers planned to retire at 65 or younger, and just 9% planned to work to 70. Now, 50% plan to stop by age 65 and 22% plan to work until at least 70. Furthermore, “Even with the planned delay in retirement, three in four expect that either they or their spouse work for pay after they retire.”

Greenwald said that this represents a “change in the very life course” for many people. “The goal of retiring reasonably young and enjoying retirement when they’re, as they say, ‘young enough to enjoy it’ is being replaced by an expectation by many of working to an age that has been considered by many to be fairly old.”

That’s a consistent theme among workers, too, according to Burrows. “Where advisors can be very helpful when they build a long-term plan is to not necessarily depend on being able to work in retirement as the backbone of their retirement strategy. Let that be a bonus to a retirement strategy.” Burrows noted that more than 60% of retirees indicated they couldn’t work in retirement for their own personal health reasons or those of a family member.

A Gallup survey conducted last spring found that, on average, current retirees left the work force at 61.

VanDerhei said that with proposals to alter the limits and tax preferences currently provided to workplace plans this year, respondents were asked how they would respond if the law was changed so they could no longer contribute to retirement plans on a pre-tax basis. “Perhaps responding to their already expressed sense of shortfalls or concerns about the future tax environment, two-thirds say they would continue to contribute at their current rates, though 10% indicate they would reduce the amount they contribute and 5% say they would quit contributing altogether,” he said.

EBRI released the 2014 Retirement Confidence Survey, conducted in January by Mathew Greenwald & Associates, on Tuesday. The survey is based on information gathered in 20-minute phone interviews with 1,000 working Americans and 501 retirees.

Sunday, March 23, 2014

Fate of Madoff employees in hands of the jury

The nine-woman-three-man jury started deliberations after U.S. District Court Judge Laura Taylor Swain gave them final legal instructions on the 31-count indictment against the former co-workers.

Juror No. 2, a man, briefly covered his face with his trial notebook after the judge appointed him as the jury foreman.

The proceeding, now among the longest white-collar crime trials in Manhattan federal court history, covers the first Madoff-related cases to be weighed by a jury. The mastermind of the Ponzi scam that stole an estimated $20 billion from thousands of investors pleaded guilty without standing trial after the scam imploded in December 2008.

Madoff, now 75, is serving a 150-year prison term at a federal penitentiary in North Carolina. The ex-employees face decades behind bars themselves if the jury finds them guilty on charges they knowingly participated in and profited from the fraud.

The defendants include Daniel Bonventre, 67, the former back office manager of Madoff's investment advisory firm; Annette Bongiorno, 65, who handled the financier's top clients; JoAnn Crupi, 52, who oversaw the company's bank account; and former Madoff computer programmers Jerome O'Hara, 50 and George Perez, 48.

They pleaded innocent and insisted throughout the trial that they were unwittingly hoodwinked by Madoff into performing job assignments that enabled the scam to run for decades.

The judge's instructions included legal guidance on the concept of "conscious avoidance," which she defined as someone deliberately closing their eyes "to what would otherwise be obvious to him or her."

Bonventre and Bongiorno took the stand in their own defense, a decision that enabled them to express their contentions directly to jurors — but also exposed them to cross-examina! tion by prosecutors. Keenly aware of that legal risk, the other defendants opted not to take the witness stand.

Instead, much of the defense's legal strategy focused on trying to raise doubts about the nearly 40 witnesses and dozens of exhibits and other evidence presented by prosecutors.

The heart of the case for both sides was the testimony of Frank DiPascali, the Mini-me to Madoff's Dr. Evil who was a manager of the Manhattan-based company's investment advisory division. During weeks on the witness stand, the star prosecution witness testified that Madoff never did any of the financial trading promised to investors and specifically linked his former co-workers to the fraud.